Introduction

This is our tenth Article and looks at how to analyze the Balance Sheet of a company. This is our third of three articles dedicated to understanding how to analyse the key financial statements of a company and is an extension of our previous article about financial analysis in general.

Looking at our previous articles, we see that financial statement analysis is an important part of the company analysis level (that we can also apply to competitor firms to understand the industry competition better). The final goal is to create a forecast to apply our Discounted Cash Flow (DCF) analysis (subject of article 11.) to attach a specific value to the common shares we want to invest in. But there are a few steps we need to go through first. As we saw, the Income Statement (article 8.) does not actually show actual cash flows – the essential input for our DCF. So, after we have analyzed our Income Statement, we then needed to assess the Cashflow statement (article 9.) as the actual input for our DCF model. The Balance Sheet (this article 10.) will be taken into consideration to assess the risk of the forecast that we input into our DCF – everything is connected.

Again, to illustrate our approach, we will use a common-form representation of the financial statements of Alibaba Group Holding Limited, which is registered with the Securities and Exchange Commission (SEC) in America. This statement is shown in full in Schedule I of this article.

Financial analysis: our roadmap to DCF (revisited)

The Income Statement and Cash Flow Statement had a close relationship to each other. Both were a measure of ‘financial flows’ over the previous year. The Income Statement, based on accrual accounting, allowed us to assess concepts of growth in sales, various profit margins and operating efficiency. The Cashflow Statement looked at how the actual cashflows occurred and when they occurred over the last year. It looked at some of the same issues from the Income Statement but also looked at the financial flows, and hence liquidity, of the company.

The Balance Sheet has some fundamental differences from the two other statements, however. First, it is not for a period of time (a year or a calendar quarter) but, rather, at a point in time, the end of the reporting period. We see that Alibaba’s financial year ends of 31 March of each year. So, the Income Statement and Cashflow Statement would be from last year’s 1 April until this year’s 31 March. But the Balance Sheet shows figures only for the day ending 31 March of the current year. It does not measure ‘flows’ over the year but rather the ‘stock’ at the end of the year.

Return and risk and financial statements

Since our first article we have emphasized that an investor has to look at both the expected return of an investment and the risk associated with that investment. In approaching our DCF model we can say the expected return is the future cashflow forecast we derive from our Income Statement and Cashflow Statement. Our assessment of risk is what rate of return we use to discount those future cash flows. For our company analysis, there are two important inputs to determine what this company risk is.

First, we evaluate the Income Statement and Cashflow Statement to see what the volatility of revenue and earnings are. If the revenue and earnings are highly variable from year-to-year, we say the company is volatile and higher risk, all other things being equal. This is sometimes referred to as the industry or business risk.

Second, we evaluate the Balance Sheet to determine the level of financial risk. Financial risk has two important aspects here: liquidity and the debt-to-equity ratio. Financial risk is the firm’s ability to meet it payments as they come do – to avoid default and potential bankruptcy. Liquidity is a shorter-term measure of financial risk and debt-to-equity is a longer term assessment.

Liquidity risk – short-term financial risk

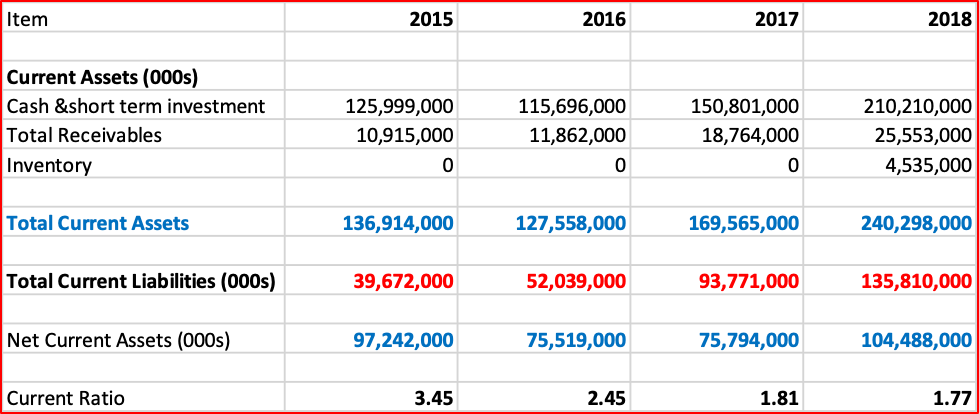

Let us do some simple liquidity analysis using the Balance Sheet of Alibaba (Schedule I).

The current liabilities of the company are all those payments that need to be made in the next year (short-term in accounting is defined as one year or less). The current assets are all those things that should be converted into cash (Accounts Receivables, Inventory, etc.) plus the actual cash balances. Comparing the amount of current assets to current liabilities give us one measure of how certain the company is to meet its short-term liabilities either from operations or existing cash balances. Note that, for conservatism, we include all Current Liabilities but not all Current Assets. There are certain items that are classified as Current Assets but not likely to be converted into cash in the near-term (i.e. Prepaid Expenses, Deferred Income Tax, etc.).

The company appears to have high liquidity (meaning low risk) as it has a large surplus of Current Assets over Current Liabilities (that can be measured either in value or as a ratio). But, look at the trend of the Current Ratio: it has been getting lower with each passing year. Does that mean the liquidity risk is going higher? Something the financial analyst would have to examine further.

We also need to examine the components of the Current Assets. Cash is already cash, but Inventory needs to be sold and the money collected before it becomes cash. As Alibaba’s balance is largely cash and small inventory, liquidity would still be considered high, even at a ratio of 1.77X.

Leverage – long-term financial risk

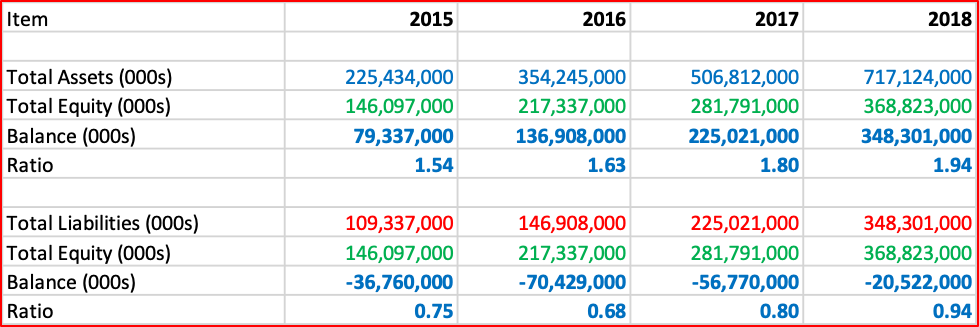

Let us also use Schedule I to look at Alibaba’s ratios on this assessment.

There are many common ways to measure longer term financial risk:

Looking at the second example, we see Alibaba has more equity than total liabilities. That would be considered quite conservative and low financial risk. But, as we saw in the liquidity risk section above, the ratios are deteriorating; in 2015, total liabilities were only 75% of equity whereas in 2018 they were getting close to 100%. Again, this negative trend would need to have much more analysis.

Risk Assessment to discount rate

With the above information about our (very brief) financial risk assessment of the company, we can now go to our final step: using this financial risk assessment to decide what an appropriate discount rate should be for this company’s expected future cash flows. In financial analysis we also use a lot of ‘relative analysis’, comparing a company to similar companies (in the same industry). We know that Alibaba is a tech company (SIC CODE 7389 – Business Services, Not Elsewhere Classified) that was listed on the NASDAQ in 2014.

According to one major financial news providers, Alibaba’s ‘peer group’ is comprised of the following firms:

So, we would carefully examine the financial ratios (and a lot of other information) on these companies and see what discount rate their equity is trading at as a check to what we calculate.

Over the last five years the NASDAQ has returned about 10.97% return per annum. This is a calculated weighted average of all the stocks in that Index, including Alibaba. So, the first question is, is Alibaba more risky than the average of stocks or less risky? One major financial firm that I follow has calculated the Beta of Alibaba to be 2.31. As the value is well above one, this implies that Alibaba is more volatile (risky) than the Index as a whole. This first suggests that a discount rate of Alibaba should be something above 10.97%. To fine tune this we would need to carefully look at many more similar firms and see what they were trading at and the implied discount rate.

Just for the record, at the time of writing, some market analysts were suggesting a rate between 18 & 20% as a discount rate. However, a detailed explanation of how to get to that precise figure is beyond the scope of this article. But, to summarize the above and the last two articles:

Concluding remarks

Financial analysis is a complex subject that requires a systematic approach to the analysis of data and markets. The top-down, four stage model introduced in a previous article is a common approach taken by equity analysis, though there are other models as well. This article looks at our third step of company financial analysis by reviewing the Balance Sheet. The next article will close off this mini-series with discounted cash flow analysis (article 11) to reach our valuation objective.

*****

Having a systematic approach to financial analysis and investing is important, it ensures consistency in analysis and decision making. There is a great amount of information in the market but taking the approach in this article (and the following four articles) gives you a way to manage all this information and synthesize it in an effective way. Yes, financial analysis can be difficult and time-consuming, but there are no easy ways to make good decisions in complex situations. It requires a sound method, time and experience.

John D. Evans, CFA (author) has over 24 years’ experience in the international capital markets working with issuers of securities and investors around the world. He has designed and taught Master’s programmes in investment management at universities in the UK and China. He was most recently Professor of Investment Management at XJTLU in Suzhou. He now manages SEIML, a consultancy to early-stage companies in China.

Jina Zhu (translator) did her Master’s in Economics in France and is fluent in Mandarin, English and French. She also works at SEIML supporting early-stage companies grow and raise capital in China.

20 May 2019