Welcome to this monthly series with Dr Francois Fong of Neo-Health Group in Hong Kong, which deals with issues related to sexual health. We hope it will contribute to public education about sexual health and help viewers, both women and men, learn about prevention and treatment for the benefit of their own health.

Today’s topic is how NHG can provide risk mitigation services to insurance providers.

Script of Interview

Interviewee Dr. Francois Fong (FF)

Position Managing Director

Company name Neo-Health Group (‘Neo-Health’)

Company website https://www.neohealth.com.hk/

Interviewer John D. Evans, CFA (JE)

Interview conducted on 28 Jan 2023

JE Welcome to our viewers of SEIML Ventures for this monthly series with Dr. Francois Fong of Neo-Health Group in Hong Kong, which deals with issues related to sexual health. We hope it will contribute to public education about sexual health and help viewers, both women and men, learn about prevention and treatment for the benefit of their own health. Today’s topic is something a little bit different, not about a specific medical issue, but rather how Neo-Health Group can provide risk mitigation services to health insurance providers. So, on that note, welcome back Francois.

FF Good to see you again, John.

JE Okay, so this is a little bit of a different topic. So, let’s start off and give a bit of background for the viewers. What is the issue for the health insurance industry with regards to people and sexually transmitted diseases?

FF In general, there’s still a lot of stigma relating to sexually transmitted diseases, especially with insurance companies. A lot of Hong Kong insurance companies or policies, they will have a specific exclusion term about sexually transmitted infection. And so a lot of people will feel also embarrassed when they have sexually related problems. When they see a doctor they often feel embarrassed or even avoid seeing doctors because of their embarrassment.

JE Okay, now let’s get into a very specific case. And tell us a little bit more about the insurance industry, life and health, and how it deals with people with HIV.

FF People living with HIV in the past, they faced a lot of problems, including getting insurance, life insurance or medical insurance. No matter whether it is a life insurance or critical illness, most people living with HIV are excluded by insurance companies. However, there seems to be a little bit of change nowadays, but because of the past, there’s still a lot of concern about people who have HIV, their life expectancy is lower, they have other medical conditions which make them at higher risk. So for medical reasons most policies would exclude people with HIV and same for life insurance.

JE Okay, so now talking more generally, what can be done to increase access to insurance for people with STDs, while at the same time managing the risk for the health insurance or life insurance provider?

FF Things have changed a lot in the last 10 to 20 years, especially for HIV. So as long patients are taking their medications regularly, they receive regular medical checkups, their life expectancy is very similar to people without HIV infections. And the risk or other medical condition is also very similar to people without HIV infections. So nowadays, we starting to see some insurance companies are starting to open up their policy for people living with HIV. So some insurance companies are already are offering life and life insurance for people living in HIV. And also we see some policies actually cover for people with HIV for their treatments. So I think there’s some changes with some insurance companies already. But I think that should be more generalized to cover more people and so that they can have broader cover.

JE So, there’s two separate issues here: there is the inclusion and providing insurance more widely to people with STDs and then, from the insurance company’s perspective, there is the risk management. So what can Neo-Health Group do to assist the insurance companies in providing coverage to sufferers of sexually transmitted diseases?

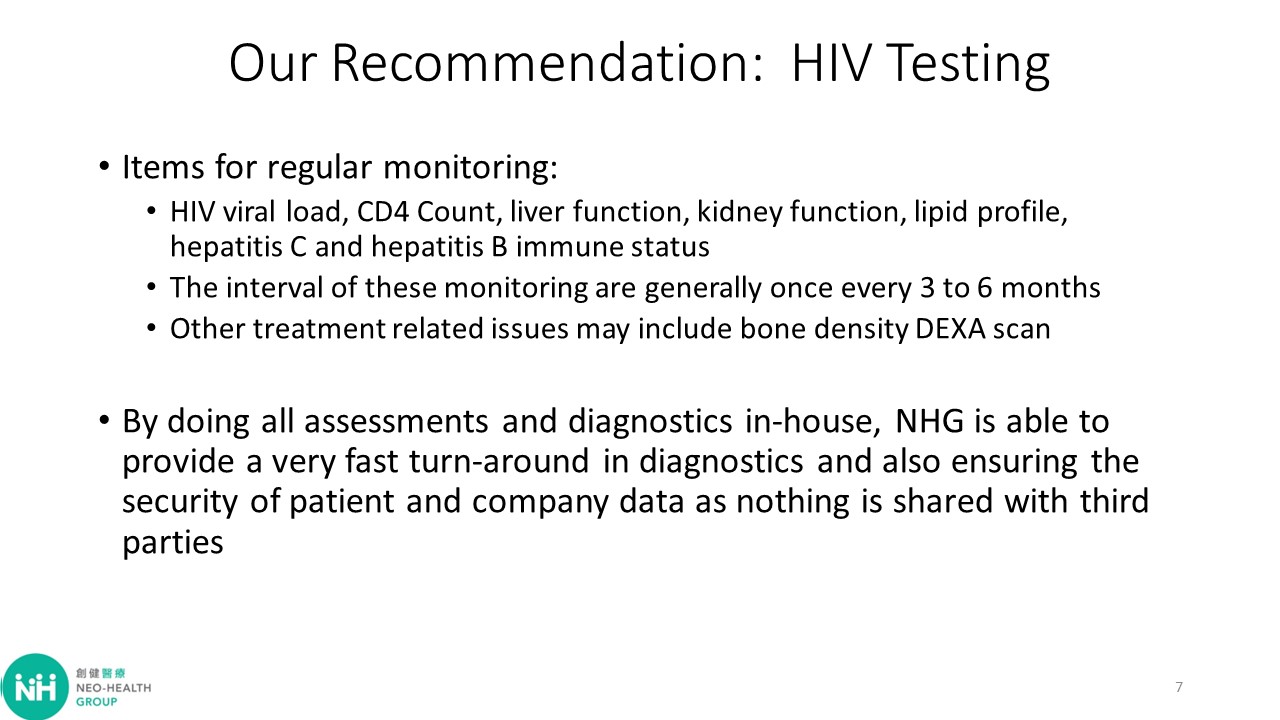

FF Well, for us directly to patients, we try to provide a more non stigmatizing environment for their sexual problems. And especially for HIV patients, we generally encourage them to receive regular checkups and take their medication regularly. So I think this group of patients, they require special care at that time. So also for insurance companies to ensure they are taking their medication regularly. So that their risk for life and also for other medical illness is lowered or approaching to people not having HIV infections. So I think regular checkup and proper care for them is very important. Rather than excluding them, is to include and providing long term care.

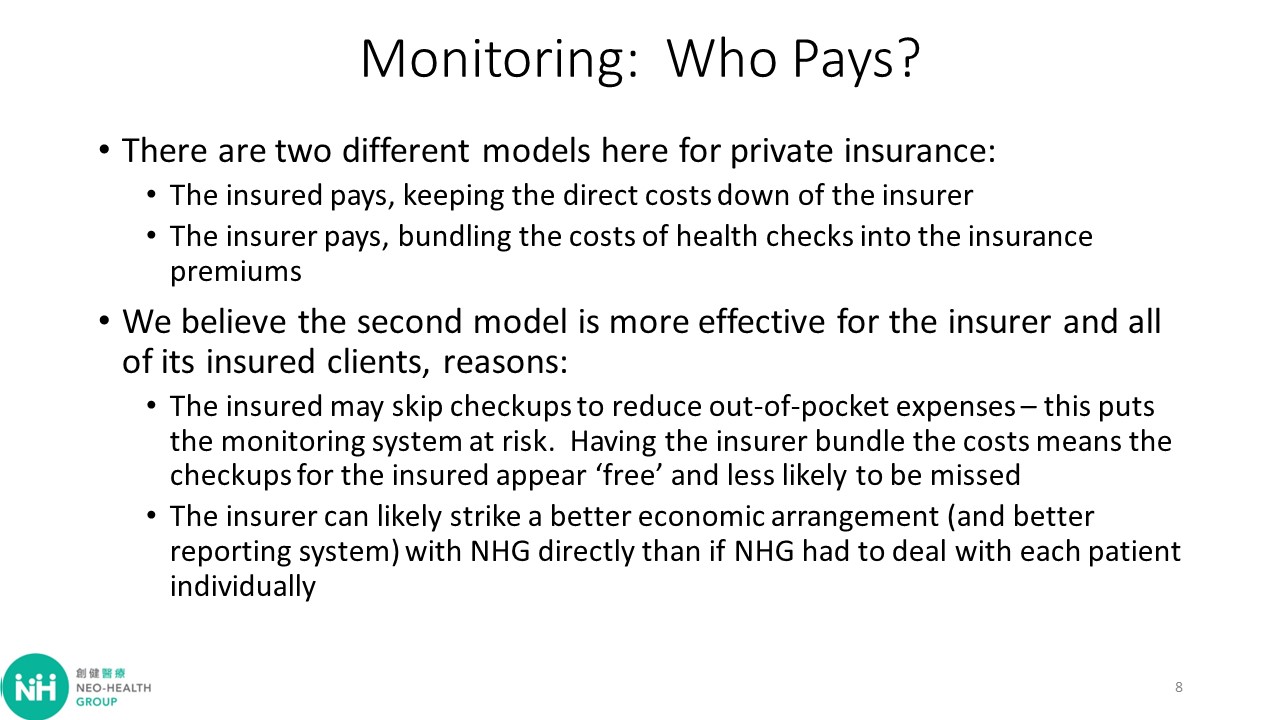

JE Okay, so I can understand how, through regular checkups, and treatment and medication, Neo-Health Group can help the sufferers who have an STD, better manage their circumstance and therefore reduce the risk to the insurance company. But then this this comes as a cost to someone, either the insurance company or the patient. So, who pays for these risk mitigation services? And why should one or the other be paying?

FF Well, I think the cost can be dealt with by the insurance company as it is a calculable risk. So as long as patients who are regularly being follow up and taking their medication, their risk is manageable. So rather than not following them, excluding them, I think now with inclusion policies and for equality it’s important for insurance companies to actually look after all patients no matter what kind of illness they have.

JE So I guess, also, that if it’s being proposed that the insurance company is directly the provider of the services and therefore bearing the cost, they can also build that into their policies, so that it’s not really a direct cost of them. But I suspect, and I’m speculating here, there’s another advantage in that, if the insurance company pays and that cost is already committed to this programme, then the patient is more likely to adhere to it than if they had to self-pay on a regular or a periodic basis. So I would speculate that this is also a more effective way to manage the programme and make sure that the treatment and risk mitigation is ongoing.

FF I agree. It is not uncommon to see HIV patients who are not wanting to review their HIV status to insurance company. And by not letting the new insurance company know, then the insurance company cannot fully assess what kind of risks they’re receiving from having a new client. So I think having an open policy is better than excluding patients with HIV.

JE Okay, my final closing question just sort of off the cuff, in Hong Kong, without mentioning any names of insurance companies, are you starting to see some or many insurance companies provide this cover to people with HIV?

FF Yeah, we have seen a few insurance companies, especially the more global insurance companies with higher premiums, or premium packages, they do cover for HIV treatment. And also for some, they will also provide life policies for patients living with HIV. I think that’s a good change. But I wouldn’t say the proportion of insurance company coverage for HIV is more than half.

JE Okay. But if a few major players are doing it, then that creates a competitive situation that other insurers who are not providing this coverage have to look at otherwise they may get left behind in terms of how the market is moving. So that’s very interesting. So that’s a little bit of a different topic. I appreciate your thoughts, but it’s very, very important because so much of health coverage is through private medical health insurance policies these days. So the interaction between professional clinics like yours, the patients, and the health insurance company, that sort of triangle is really important. So thanks for giving us this update today for as well.

FF You’re welcome, John.

End.